RBI Watch

Posted by Prabir Sorkel | August 14, 2025

RBI & Co-lending: Concerns unheeded

The RBI has come out with its final rules on co-lending arrangements. There are a few changes from the earlier draft. Like now both sides are required to retain a minimum 10% of the individual loans in its books. And now even two NBFCs and two banks can get into co-lending arrangements. Those who are excited belive that now NBFCs will be better positioned to tap into cheaper bank funding to serve markets previously underserved. But sceptics have been rightly challenging the fundamentals of co-lending arrangements between private NBFCs and public sector banks as it entails cheap public sector bank money in the hands of profit driven usurious NBFCs who are notorious for their high rates and bad recovery practices. We are effectively be leaving the most marginalised – farmers, MSMEs – in the hands of loan sharks that too with public money. Given that big corporates are still not allowed banking licenses, this is nothing but a backdoor entry.

We fare well in Digital Payment Index, but concerns around fraud rise too

In RBI’s latest Digital Payment Index, we have climbed up to 493 from 465 last year. While the digital thrust has been claimed as a feather in recent years, but such claims also need to be qualified by the fact that India lost Rs 22,842 crore to cybercriminals and fraudsters in 2024 as per DataLEADS, a Delhi-based media and tech company. Indian Cybercrime Coordination Centre, I4C, predicts that we will lose over Rs 1.2 lakh crore this year. Bank frauds value has nearly tripled in FY25 driven by loan and digital payment scam. Just last week a Gujarat doctor lost 19 crores to digital arrest scam, a phenomenon that has spread like wildfire. While there are advisories and cautionary notes from the RBI advising customers to be careful, but this needs more converted attention and thinking.

RBI Bulletin: Concerns around Manufacturing, Sale & Demand

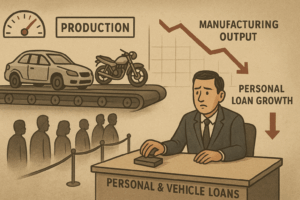

The State of the Economy in the latest RBI Bulletin states that as far as manufacturing is concerned, among the use-based categories, primary goods, consumer durables, and consumer non-durables recorded a decline. One of the indicators about the appetite of demand in the economy is of course automobiles. Of that, the RBI says that production has slowed “dragged down by passenger vehicle and two wheeler”. The other related indicator of course is the credit landscape. The RBI Bulletin shows that personal loans, which is the main driver of banks’ credit growth, also recorded a sharp deceleration, which is also dragged down by vehicle loans, other personal loans, etc.